Duty Under Management: The CFO Question That Reveals a Governance Gap

A CFO’s question about ‘duty under management’ exposes something many businesses don’t see until scrutiny arrives: customs may be functioning, but not fully explainable end-to-end. With data fragmented across brokers, systems and teams, organisations can often describe parts of their customs activity but struggle to present a coherent picture of what’s been paid, mitigated, saved and exposed over the historical look-back period. This piece sets out what explainability really means, why it is a governance issue (not a technical one), and why improving visibility supports better commercial decisions.

Can You Explain It?

Imagine a new CFO joins the business. Early on, they ask a seemingly simple question:

“How much customs duty do we have under management?”

Not just how much duty is paid, but the full picture:

- What’s paid/ What’s mitigated?

- What’s been saved through free trade agreements, special procedures or reliefs?

- What sits within the historic look-back period.

It’s a reasonable question to ask your team.

Why This Is Harder To Answer Than It Should Be

In many organisations, customs “works”, but it isn’t fully visible. Data is fragmented across brokers, finance systems, procurement decisions and supply chain operations. Responsibility is distributed. Execution is often outsourced. And over time, the focus shifts to keeping goods moving, rather than understanding the position end-to-end.

As a result, businesses can usually explain parts of their customs activity, but not the whole. When asked to describe their duty under management, many realise they’ve only ever looked at duty paid, not duty actively managed.

What “Being Able To Explain It” Really Means

Explaining a customs position isn’t about technical detail. It’s about coherence. At a minimum, it means being able to articulate:

- Where customs data comes from, and how reliable it is

- Who is responsible for what and where ownership genuinely sits

- How an import moves through the business, from procurement decision to clearance to onward sale or export

- What assumptions and ultimately evidence underpin duty costs, savings and mitigations

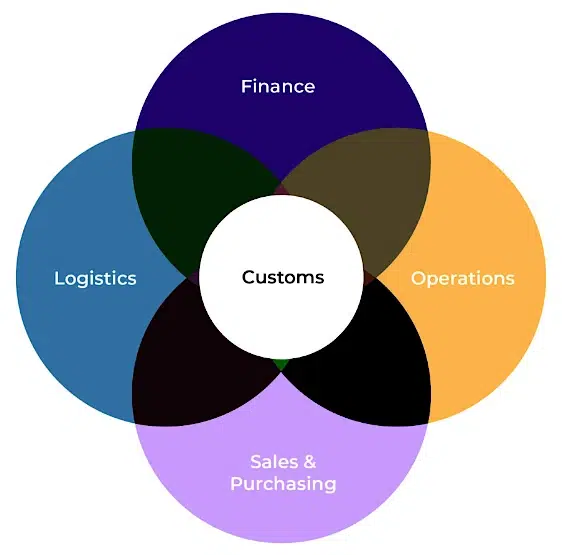

Customs sits at the intersection of finance, procurement, supply chain and operations. Everyone owns a piece, but without a joined-up view, no one owns the whole. That’s usually where explainability breaks down.

The Cost Of Not Being Able To Explain It

When customs can’t be clearly explained, the consequences can be significant.

- Cost of sales increases because duty is treated as fixed rather than managed.

- Time is wasted stitching together spreadsheets and legacy data.

- Small inconsistencies compound over time into large exposures.

Most importantly, decision-making suffers.

Without clear visibility, businesses struggle to make confident commercial choices. In an area as nuanced as customs, partial understanding can be more dangerous than none at all. Assumptions go unchallenged. Opportunities are missed. Risk is misunderstood.

Why CFOs Tend To Ask This Question Early

This is often why a CFO shows such interest in customs early on.

Customs obligations sit squarely within financial governance. Under the Senior Accounting Officer rules, accountability cannot be fully delegated. A CFO who has seen the impact of a difficult audit elsewhere will instinctively want to understand how things really work in practice.

Being unable to clearly explain the customs position is not a technical failing. It’s a governance gap.

A Better Conversation To Have Now

The point isn’t to criticise how businesses manage customs today. Most are doing their best with the structures they have.

But there is real value in asking the question internally before it’s asked by HMRC:

- What is our duty under management?

- Where does responsibility truly sit?

- Could we explain this calmly and confidently if asked?

If gaps appear, it’s far better to surface them early, whether through internal review or independent support, than to discover them under pressure. Transparency creates options to strengthen controls, address risks, and identify opportunities.

Better visibility leads to better commercial decisions.

Tools and data can help provide that visibility quickly, and many businesses are now using technology to gain deeper insight across historic and current customs activity. But the starting point is not the tool, it’s the willingness to ask the question honestly.

Customs that works is not the same as customs that can be explained. If you can’t explain it simply, does your team really understand it?

Want Clearer Customs Visibility?

If your duty position is difficult to explain end-to-end, Barbourne Brook can help you establish a clear view of duty under management, map ownership across teams, and strengthen the evidence trail and controls that underpin confident decision-making and audit readiness. Get in touch here.

Contact Our Team …

Related Posts

‘My Broker Told Me To Do It’: Why That Defence Won’t Save You At Tribunal

It is one of the most common things we…